With the recent discovery of vast quantities of natural gas it is now honest to say that we are in the midst of an energy transition not in an energy crisis. This is a wrenching change in the kinds of energy we use and the ways we produce them. However there has not been enough discussion of how we can help companies make smart decisions around whether to retrofit their existing coal plants. Fossil fuels produce 95 percent of the carbon emissions and the electricity sector accounts for 33% of carbon emissions. The critical decision we need to focus on now is whether individual companies should retrofit their coal plants or whether there are lower risk and more economic alternatives.

We live in a free market so therefore we rely on market participants voluntarily making correct decisions that are economically sound and in sync with the larger set of stakeholders such as the government and the desires of the people at large. Coal retrofit is the single biggest imminent decision we need to address if we are to get on the correct road to long term success. We need to work on solutions that make market sense and that make policy sense so we head in a direction that optimizes the value for all stakeholders.

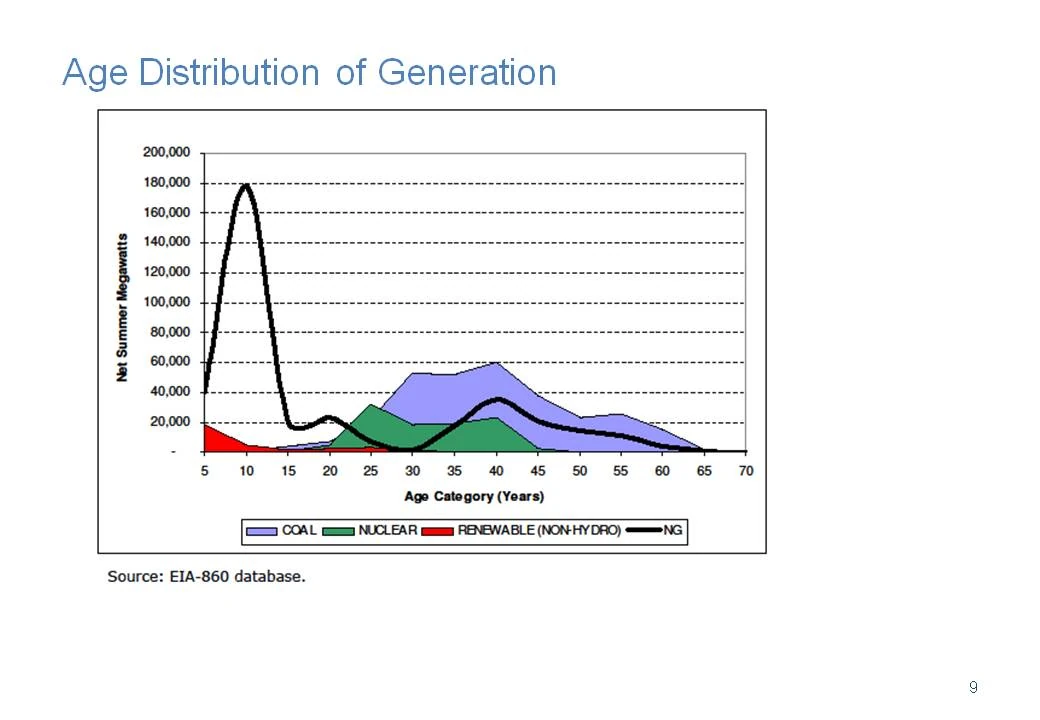

The starting point for our discussion is the simple fact that the US coal generation fleet is aging rapidly.

{kind=link}

US investors are reluctant to invest in coal retrofits due to significant perceived risk. Indeed even large players with billions in assets are finding it difficult to fund coal retrofits and new coal plant construction. The investor reluctance is coming from several areas of perceived risk…

1. Cost risk of known EPA upgrades which could be up to $500k/MW of capacity

2. Future cost risk associated with unknown EPA upgrades associated with GHGs

3. Future cost risks associated with CO2 which could be up to $50/MWhr. California is already implementing a carbon market for instance and Europe too is already trading carbon.

4. Future market risk of “Dirty fossil power” – renewed long term PPAs may be a challenge as consumers perceive coal power as “dirty”

The result is that many significant investors are in a “wait and see” attitude. The issue for the future is what is the best direction to proceed if coal is perceived as too risky. Unfortunately it seems like clean coal is moving too slowly and is still too costly and soon it could be that coal projects may become “unfinancable”.

However the waiting game cannot last forever. In the next few years investors need to make significant bets on which way to go on coal retrofits.

If we assume for the moment that it is true that coal is now a high risk option both financially and politically, then what are our alternatives.

It is in the area of alternatives that we need to be careful. A recent Discover magazine article on 4 bold ideas to make America’s energy supply safer, cleaner and virtually inexhaustible is a case in point. The big ideas are fantastic. Brilliant options are discussed such as “downsized” modular nuclear power and endless natural gas from gas hydrates along the coasts of continents (the energy potential of hydrates is vast Amadeu K.Sum director of the Center for Hydrate Reseach at Colorado State of Mines twice “Twice as much as .. all the fossil fuels on the planet”). However these big ideas may not be of much immediate help to investors trying to make optimal decisions in the short term. Investors are reluctant to add technology risk to their list of concerns. We should probably at least for the purposes of this discussion stick with technologies that are proven players today and upon which lower risk decisions can be made. Energy investors are typically looking for lower risk investments with fixed returns. This may be a short sighted approach to many. The fact is though that risk must be managed. Venture capitalists fund innovations, however typical energy investors look for safer options. We are of course in no way saying that the “big ideas” are not the future. Technologies such as modular nuclear may evolve rapidly and come to dominate the market. However right now for example it looks like the first modular nuclear plant to be built by TVA will not be operational till 2020 in the US. Innovations in silicon wafer technology could reduce the cost of PV panels by 60%. This innovation discussed in the Discover article could reduce solar power costs from today’s $120/mwhr to $40/mwhr! However as promising as these innovations are, many key investors will prefer to wait until the technology is mature before plunging in.

So what are our major alternatives from this perspective?

In this context we have identified three alternatives:

1. Gas generation

2. Wind

3. Gas and Wind hybrids

Each has their pros and cons. We will introduce them and discuss them as well as introduce a “market price based” approach to comparing them. In our following section we will plunge more deeply into the guts of the economics but for now we will start with an overview of the contenders.

Gas Generation

Gas generation already accounts for 25% of our electricity supply. In addition there has been significant growth in gas capacity in the recent past. In addition gas on average produces less than half the CO2 of the average coal plant per MWhr produced.

{kind=link}

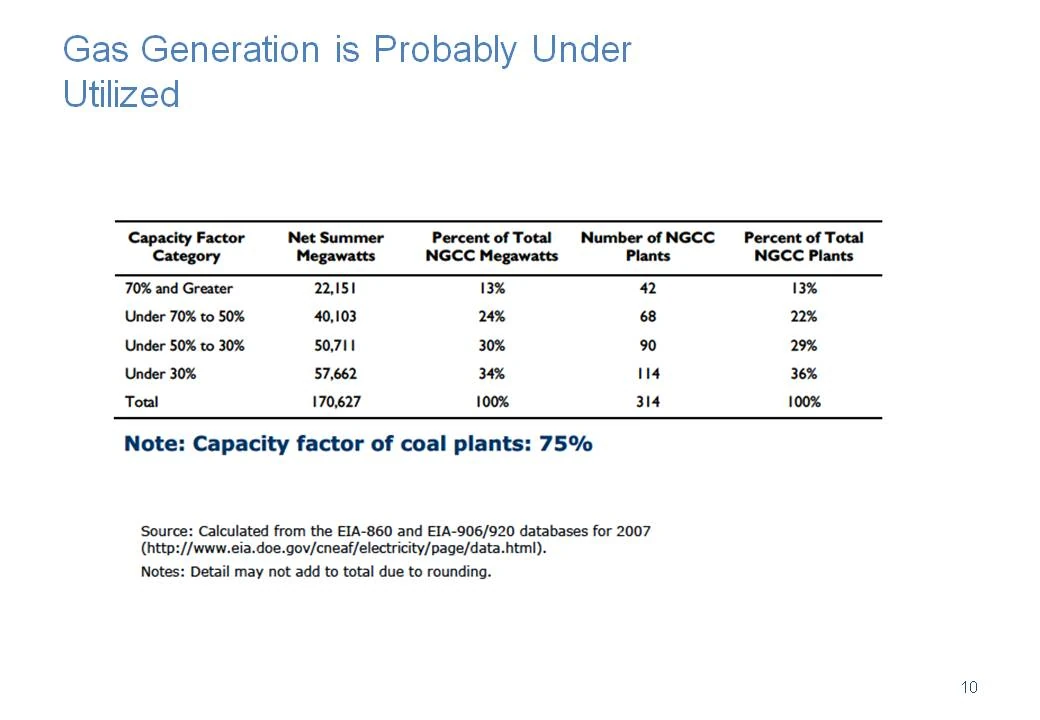

To many it seems that gas is the clear alternative. In addition it seems that current gas capacity may be under utilized.

If gas is under utilized then increasing gas utilization may be an excellent way forward. This is already happening.

For example this process has already been under way for several years in the PJM market. Gas has already been pushing inefficient coal plants out of the markets. The EPA rules will acclerate this process most likely. According to PJM’s report on the impact of EPA rules…

Over the past four years, the combination of reduced natural gas/coal price spreads and lower demand have already resulted in lower capacity factors that have fallen from 65 percent in 2007 to about 40 percent in 2010 for coal-fired units less than 400 MW and more than 40 years old.7At the same time coal-fired units greater than 400 MW, regardless of age, have maintained relatively constant capacity factors in the face of reduced hourly demands and reduced fuel price spreads.

Overall, the decline in the gas/coal price spread and average hourly demand have resulted in declining net energy market revenues for all coal capacity, but net revenues remain lowest for coal-fired units less than 400 MW and more than 40 years old. The spread between coal and natural gas prices has fallen significantly, from over $5.00/mmBtu in 2006-2008 to $2.50-$2.80/mmBtu in 2009 and 2010.

As forecasted by the Energy Information Administration in its 2011 Annual Energy Outlook the spread will remain below $3.00/mmBtu through 2015. The decreasing coal-natural gas spread means lower net energy market revenues for all coal units, including large, base-load coal units, in every hour they operate. For smaller, older coal units that are less efficient, they may actually be displaced by natural gas units in addition to earning smaller margins when they do operate

Coal units less than 400 MW and more than 40 years old only account for 29 percent of the PJM total (almost 23,000 MW), but account for more than half of the capacity without one or more of the necessary SO2 or nitrogen oxide retrofits to comply with CSAPR and NESHAP.

Gas seems right now to be the real winner in coal retrofits. Indeed according to PJM…

In total, there is over 14,000 MW of installed coal-fired capacity that already appears headed toward retirement largely due to EPA rules. This initial market response to the EPA rules is more than 25 percent greater than the 11,000 MW of capacity requiring more than Net CONE to continue going forward suggesting additional capacity requiring between 0.5 Net CONE and Net CONE may elect to retire rather than retrofit.

In addition PJM notes

Even with almost 7,000 MW less coal capacity clearing for the 2014/2015 Delivery Year, PJM estimates the RTO will carry a reserve margin of 19.6 percent for the Delivery Year, including the demand and capacity commitments of FRR entities.16 Even with the potential retirement of coal capacity already announced by FRR entities, there are also announced commitments to replace a portion of that capacity with new gas-fired capacity such that the RTO would still carry a reserve margin at or above of the target 15.3 percent installed reserve margin. Add into the mix the potential for new entry from Demand Resources, as has been the trend in recent years, and resource adequacy does not appear to be threatened

Is gas just the outright winner? Is there a possibility of new approaches that will provide strategic advantage over coal retrofits both in the short, medium and longer term?

If we assume for that moment that to most financiers that coal may be becoming perceived as more of a liability than an asset, what are the realistic alternatives?

Wind

An often quoted answer to the wind reliability issue is that “It is always blowing somewhere” and all we need is a “super grid”. Unfortunately we don’t have a super grid and we don’t have time to wait for one. Financiers need realistic solutions. Unfortunately “it is always blowing somewhere” does not get us anywhere in terms of finding a realistic alternate to coal. One of the reasons we quoted the MISO study on “How variable is wind” was to to show quantitative data from a major ISO that shows that wind alone is not a reliable energy source. That does not mean that wind is not valuable. It is highly valuable. However for renewable supporters – the best = “All Renewables” could well be the enemy of a good solution that matches renewable and non renewable energy. The wind industry does not serve itself by espousing the “it always blows somewhere” mantra.

To many in the industry wind alone does not seem to be the answer. As discussed in “the true cost of wind” and in “how variable is wind” there are significant drawbacks to considering wind as a standalone generation solution, especially given that wind does not align well with seasonal demand in the US.

Is gas just the outright winner after all? Is there no possibility of new approaches that will provide strategic advantage over coal retrofits both in the short, medium and longer term?

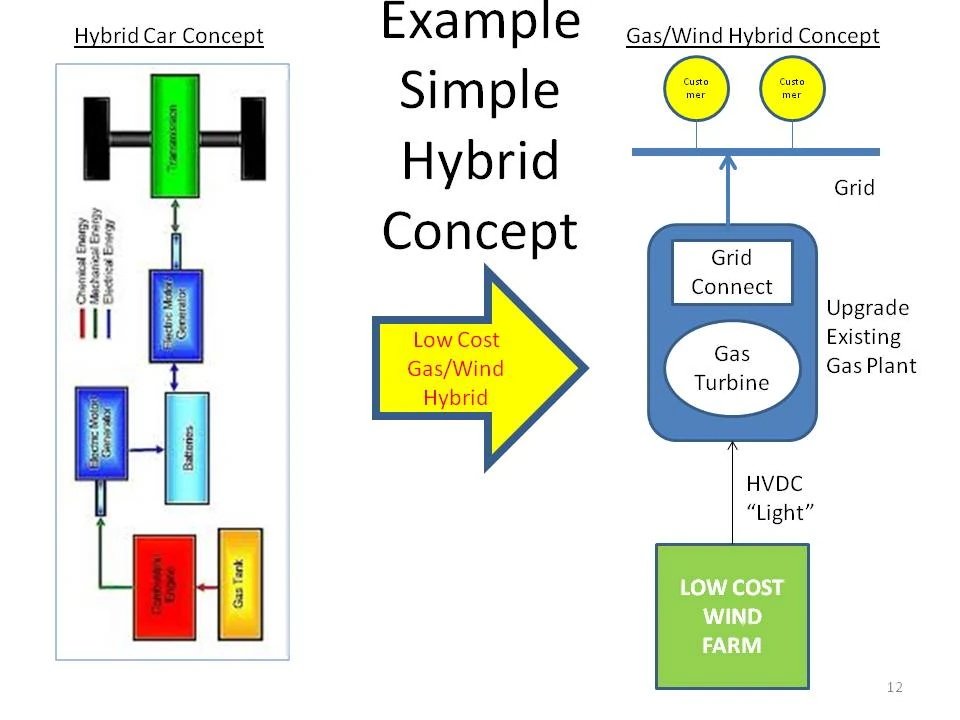

Gas/Wind Hybrids A potentially superior Solution?

{kind=link}

Gas wind hybrids are simply the combining of gas an wind generation. An example of which is the Lea County Electric Coop project in New Mexico. In this project gas and wind have been matched together.

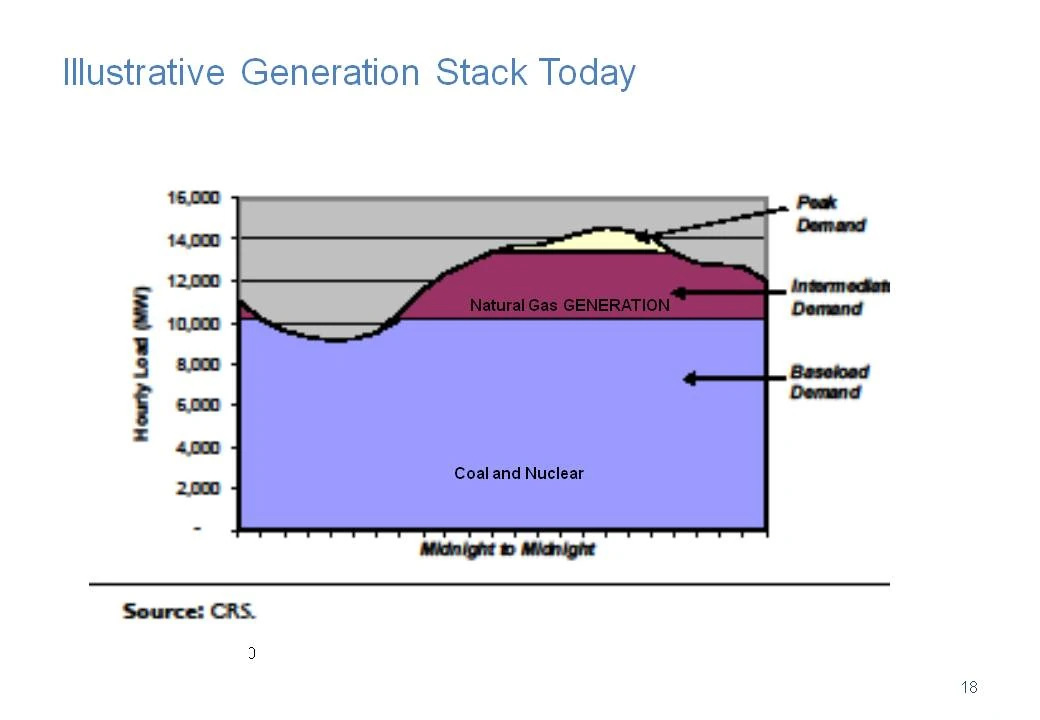

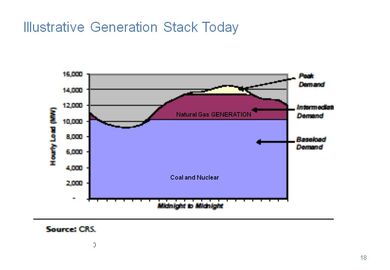

The traditional energy products are like the following.

{kind=link}

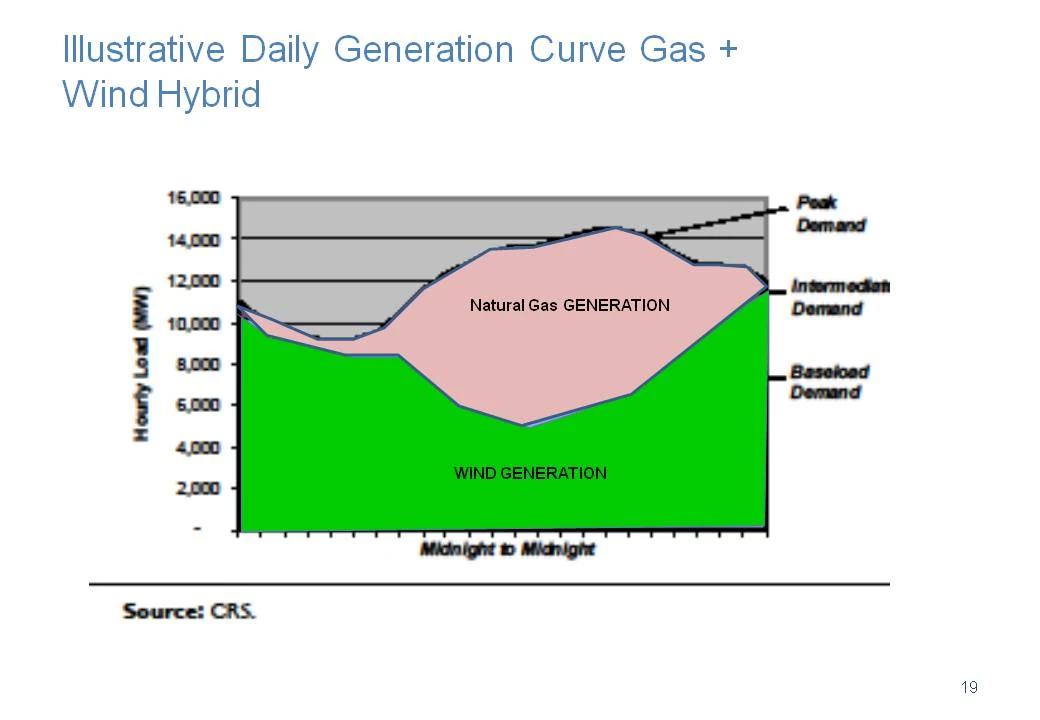

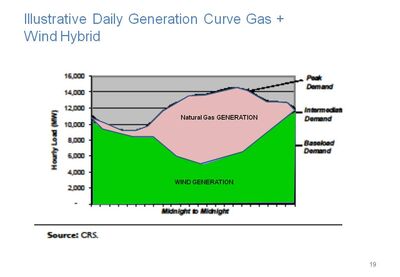

An illustrative hybrid generation output would look as follows

{kind=link}

But is gas/wind hybrids a realistic alternative? We discussed the possibility that gas and renewable not just gas was a potential solution in a previous section.

If we assume that wind alone is not a realistic alternative we are left with gas vs. gas/wind hybrids.

The key now is to perform a proper analysis of gas generation vs. gas/wind hybrids. To do this we will need to understand the price risk components. While many price components like ancillary services are hidden and charged to loads, let us assume we were to allocate these costs back to the generators for the gas wind hybrid. Some of the major price components are then as follows.

· - Energy costs

o Fixed costs

§ EPA retrofit costs

§ New Plant Costs

§ CO2 retrofit costs

§ Reserve Margin

o Marginal costs

§ Fuel

§ O&M

§ Production subsidies

§ RECS

§ CO2 costs/ton

§ Ancillary service costs

· - Congestion costs

· - Losses

· - Transmission costs

· - Grid operation costs

We will evaluate these alternatives in more detail in following discussions. After all is not our objective to come up with an optimal economic and socially acceptable way forward? Even the most dogmatic conservatives and progressives should agree on that simple idea!